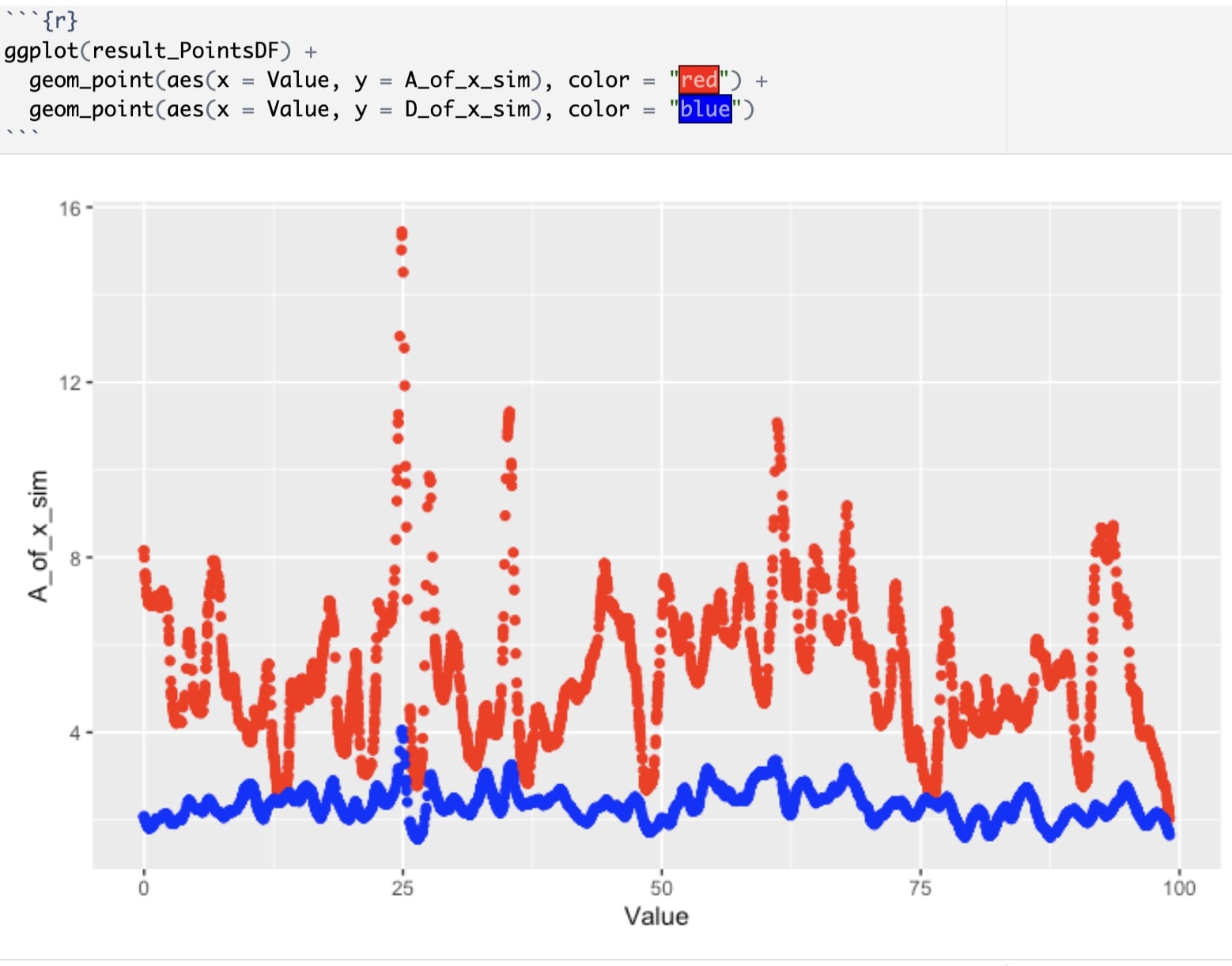

Financial Market Behavior Modeling

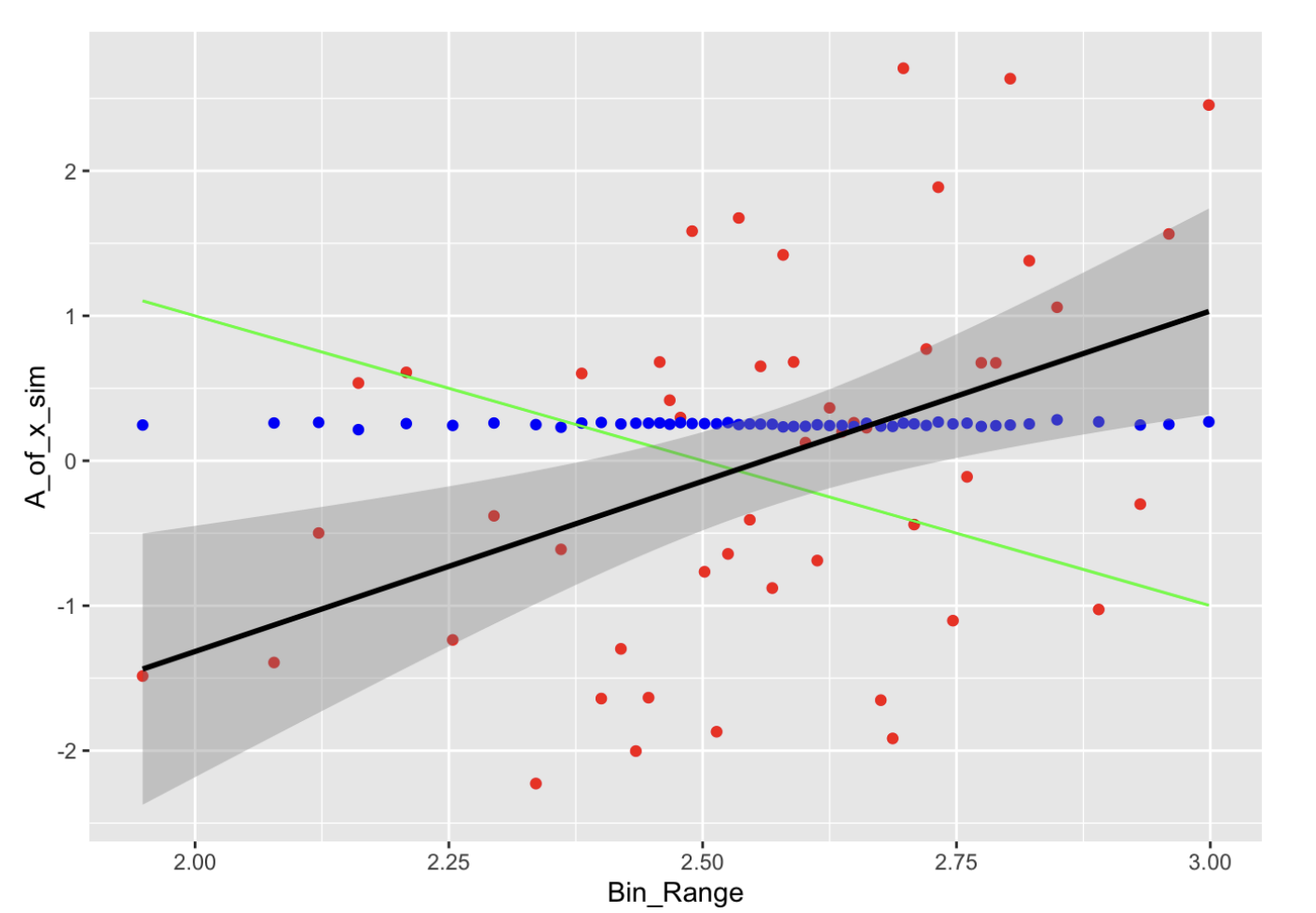

Applied theoretical physics and stochastic differential equations, incorporating research from Non-parametric estimation of Stochastic Differential Equations from stationary time-series (https://arxiv.org/abs/2007.08054), to develop a computational model for financial market behavior. This enabled improved forecasting of asset price dynamics and volatility.

Strengthened my skills in mathematical modeling, data wrangling, and algorithm implementation, gaining experience in quantitative analysis and stochastic processes. For any references, please reach out to Professor Sarah Marzen - https://www.sarahmarzen.com/